[.green-span]How Data-Driven Loan Placement Improves Portfolio Performance[.green-span]

Data-driven loan placement changes that equation by using real-time borrower data, credit signals, and automated rules to match applications with lenders who are actually likely to approve them. This guide covers how data integration, intelligent decisioning, and decline waterfalls work together to improve approval rates, accelerate funding, and strengthen portfolio performance.

What Is Data-Driven Loan Placement

Data-driven loan placement uses real-time borrower data, credit signals, and automated rules to match loan applications with lenders whose criteria and risk appetite align with each borrower's profile. Instead of an underwriter manually reviewing an application and sending it to one or two familiar lenders, automated systems evaluate dozens of variables simultaneously and route applications across a network of lenders in seconds.

The difference between manual and data-driven placement comes down to precision and speed. Manual routing relies on human judgment and limited lender relationships. Data-driven systems pull live financial information bank transactions, credit scores, business context and find the best match based on actual data rather than assumptions.

- Data-driven loan placement: matching borrowers to lenders using automated data analysis rather than manual review

- Key inputs: credit data, cash flow, business financials, and risk scores

- Goal: improve approval rates, reduce time to funding, and optimize portfolio outcomes

Why Data-Driven Placement Outperforms Manual Routing

The shift from manual to data-driven placement delivers measurable improvements across the lending lifecycle. Teams using automated placement consistently report faster funding, higher approval rates, and leaner operations.

Faster Speed to Funding

Manual routing creates bottlenecks. Applications sit in queues, documents get lost between systems, and decisions wait on human availability. Data-driven systems process applications as data flows in, removing the disconnected steps that slow traditional workflows.

Pre-qualified offers hosted on Lendflow drive an average of 42% faster speed to funding. That acceleration comes from eliminating handoffs and automating the steps that used to require manual coordination.

Higher Approval Rates Through Better Matching

When applications go to lenders whose criteria they don't meet, declines pile up - the Federal Reserve found 54% full approval at small banks versus lower rates at other lender types. Intelligent routing solves this problem by matching borrowers with lenders who are actually likely to approve them based on their specific profile.

A borrower who doesn't fit one lender's risk model might be an ideal candidate for another. Data-driven placement finds that match automatically, which improves approval rates without lowering credit standards.

Reduced Operational Overhead

Embedded finance customers using Lendflow operate with 80% smaller teams while converting similar funding volumes. That efficiency comes from automating document handling, communication, and decision support.

Instead of adding headcount as volume grows, teams can scale by letting automation handle repetitive work. The operational savings compound over time as application volume increases.

How Data Integration Powers Smarter Loan Matching

Accurate placement depends on having complete, current data in one place. Fragmented systems—where application data lives in one tool, bank data in another, and credit reports somewhere else—make intelligent routing nearly impossible.

Unifying Application and Financial Data in Real Time

Modern orchestration platforms consolidate borrower-submitted information with live financial feeds through APIs and pre-built connectors. The system sees the full picture: what the borrower reported plus what their bank accounts and financial records actually show.

A single source of truth that updates as new data arrives is fundamentally different from a static snapshot taken at the moment of application. Real-time data means placement decisions reflect current borrower circumstances.

Connecting Credit Bureaus and Alternative Data Sources

Traditional credit scores tell part of the story. Alternative data fills in the gaps, especially for small businesses with thin credit files - TransUnion found that including rent payments moved 9% of credit-invisible consumers to scorable.

Alternative data includes bank transactions, accounting software integrations, and payment history with vendors. Data-driven placement systems pull from both traditional bureaus and alternative sources to build a more complete borrower profile.

Eliminating Silos Between Lending Systems

Many lenders still operate with disconnected tools: one for origination, another for underwriting, a third for servicing. Each handoff introduces delays and data loss.

Orchestration platforms centralize data flows across the entire lending lifecycle. When every system draws from the same data layer, placement decisions reflect current reality rather than outdated information passed between disconnected tools.

Key Data Signals for Accurate Loan Placement

Not all data carries equal weight in placement decisions. Certain signals consistently predict which lenders will approve an application and which loan products fit the borrower's situation.

Cash Flow and Bank Transaction Data

Transaction-level data reveals business health that credit scores miss. A company might have a mediocre credit score but show consistent revenue growth and healthy cash reserves in their bank statements.

This granular view helps placement systems identify borrowers who are stronger candidates than their credit scores suggest. Routing decisions based on actual cash flow patterns lead to better lender matches.

Credit and Risk Scores

Traditional credit scores remain foundational for placement decisions. Composite risk scores add another layer by combining multiple data points into an explainable assessment.

The key is transparency. Lenders want to understand why a score is what it is, not just accept a number without context. Explainable scores help lenders trust automated placement decisions.

Industry Classification and Business Context

A restaurant and a software company with identical financials represent very different risk profiles. Automatic NAICS/SIC classification helps route deals to lenders with sector expertise and appropriate risk models.

Industry classification happens automatically through AI agents that analyze business descriptions and documentation. No manual coding is required, and the classification informs which lenders receive each application.

Using Portfolio Analytics to Optimize Loan Origination

Portfolio analytics refers to the systematic analysis of loan performance data to inform origination decisions. When applied to placement, portfolio analytics help lenders understand which borrower profiles perform best with which products.

Automating Document Review and Verification

Document review is traditionally one of the most time-consuming steps in origination. Underwriters spend hours extracting information from PDFs, tax returns, and bank statements.

AI-powered document analysis extracts structured data from documents in seconds rather than hours. The system pulls key fields automatically and flags inconsistencies, freeing underwriters to focus on judgment calls rather than data entry.

Applying Intelligent Decisioning Rules

Configurable decision models auto-approve, decline, or escalate applications based on data thresholds. Lenders set up rules that reflect their credit criteria, and the system applies those rules consistently across every application.

The flexibility matters because risk appetite changes. A lender might tighten criteria during economic uncertainty or expand them when entering a new market. Configurable rules adapt without requiring engineering work.

Accelerating Time to Decision

When document review, data aggregation, and decisioning all happen automatically, the application-to-decision timeline compresses dramatically—McKinsey found that agentic AI in credit processes delivers efficiency increases of 40% to 80%. What once took days can happen in minutes.

Faster decisions benefit everyone involved. Borrowers get answers sooner, lenders close deals faster, and operations teams handle higher volumes without burning out.

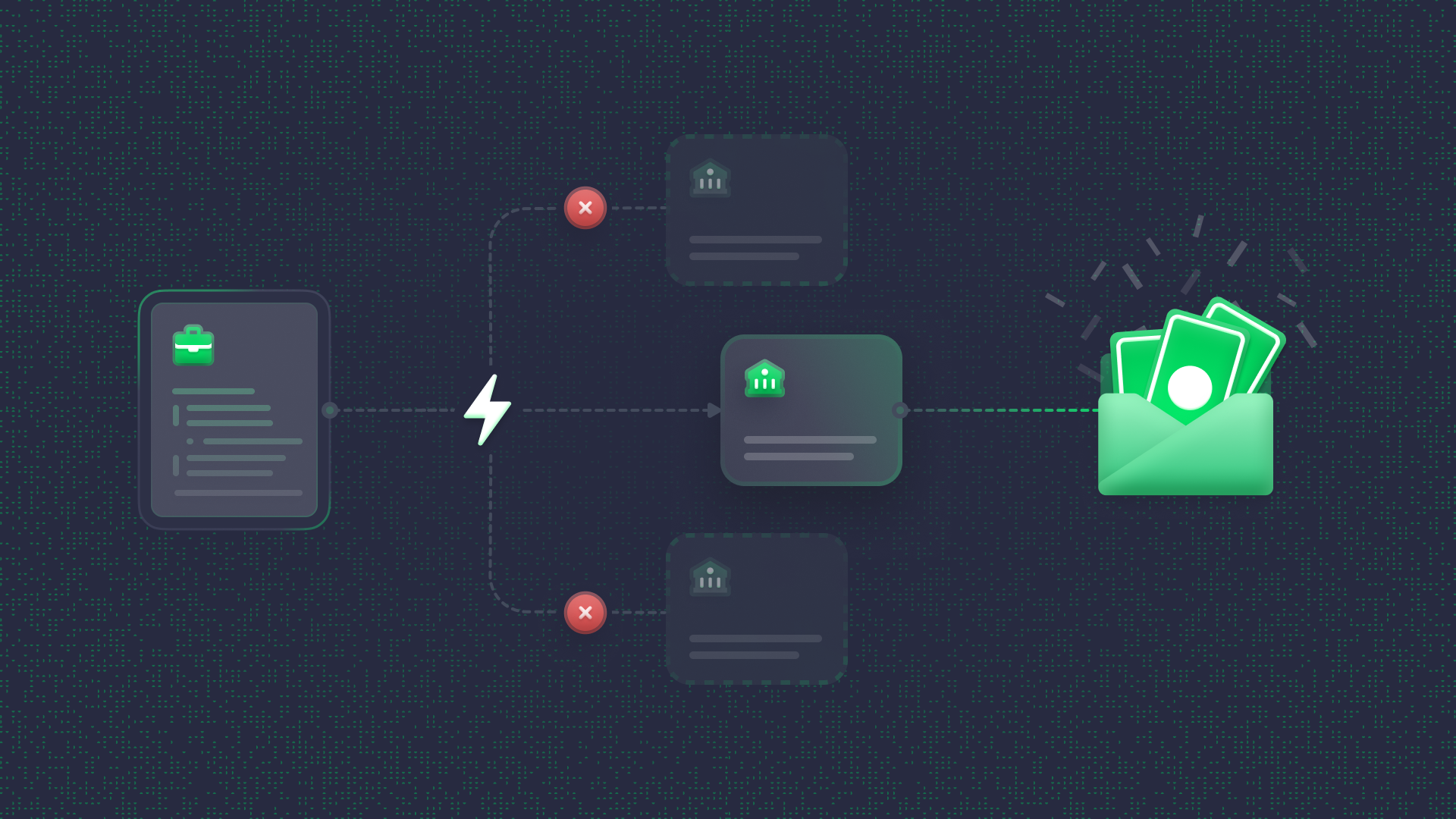

How Decline Waterfalls and Second-Look Marketplaces Improve Conversion

A decline waterfall is an automated sequence that routes declined applications to alternative lenders who might approve them. A second-look marketplace is the network of lenders participating in that waterfall.

Routing Declined Applications to Alternative Lenders

When one lender declines an application, the system automatically sends it to others whose criteria might be a better fit. This routing happens without manual intervention, and the borrower doesn't know they were declined by the first lender.

The result is more funded deals from the same application volume. Applications that would have died after a single decline get multiple chances at approval.

Configuring Rules-Based Waterfall Logic

Lenders set up merit-based rules determining the sequence of routing. Rules might prioritize lenders by rate, approval likelihood, or product type depending on the borrower's profile.

Lendflow Connect supports waterfall configuration through its Second-Look Marketplace, where 75+ lenders participate in a network designed to maximize approval rates across the full range of SMB financing products.

Maximizing Approval Rates Without Manual Intervention

Without a waterfall, a declined application often dies. With one, that same application might get approved by the third or fourth lender in the sequence.

Waterfall automation ensures no deal leaves money on the table. Applications that would otherwise be lost convert into funded deals, which directly improves portfolio performance.

Measuring Placement Success With Portfolio Performance Metrics

Data-driven placement is only valuable if it produces measurable results. Tracking the right metrics reveals whether your placement strategy is working and where it can improve.

- Default and delinquency rates: measure credit quality of placed loans

- Funding volume and approval ratios: track conversion from application to funded deal

- Cost per funded loan: assess operational efficiency gains

Default and Delinquency Rates

Better placement correlates with lower defaults because borrowers end up in products that match their repayment capacity. If defaults rise, that signal indicates placement criteria may benefit from adjustment.

Tracking default rates by lender, product type, and borrower segment helps identify which placement rules are working and which ones are producing problematic loans.

Funding Volume and Approval Ratios

What percentage of applications convert to funded loans? This ratio benchmarks placement effectiveness and highlights where applications are falling out of the funnel.

Approval ratios broken down by data signal—credit score bands, industry categories, cash flow ranges—reveal which borrower profiles are converting well and which ones are getting stuck.

Cost Per Funded Loan

Automation reduces the labor cost associated with each funded deal. Tracking cost per funded loan over time shows whether efficiency gains are materializing as volume scales.

Lower cost per funded loan means the same team can handle more volume, or the same volume can be handled with fewer resources. Either outcome improves portfolio economics.

Build a Data-Driven Loan Placement Strategy With Lendflow

Lendflow's platform brings together data integration, intelligent decisioning, and workflow automation through a single integration. Over $1.5B+ in offers have been made on the platform as of March 2025.

- Lendflow Connect: single integration to 75+ lenders with decline waterfalls and second-look marketplace

- Lendflow Intelligence: automated decisioning that transforms data into lending decisions

- Lendflow Automate: AI agents for document analysis, risk scoring, and borrower communications

The platform is SOC 2 Type II compliant and designed for fast implementation. Widgets launch in under two weeks, and full API integration takes 30–45 days.

Book a demo to see how Lendflow can help you build a data-driven loan placement strategy that improves portfolio performance while keeping your team lean.

FAQs About Data-Driven Loan Placement

What is a placement loan?

A placement loan refers to a loan that has been matched and assigned to a specific lender or investor based on borrower criteria, risk profile, and lender appetite. Data-driven placement automates this matching process using real-time data rather than manual review.

What are PD, LGD, and EAD models in lending?

PD (Probability of Default), LGD (Loss Given Default), and EAD (Exposure at Default) are credit risk models that estimate the likelihood and severity of borrower default. PD predicts how likely a borrower is to default, LGD estimates how much the lender will lose if default occurs, and EAD calculates the total exposure at the time of default. Data-driven placement systems use variations of these models to quantify risk for lender matching.

How does data-driven loan placement differ for embedded lending versus direct lenders?

Embedded lending platforms route applications through brand partners to multiple lenders via a single integration. Direct lenders use data-driven placement internally to optimize their own underwriting and portfolio allocation. Both benefit from the same underlying data and decisioning capabilities, though embedded platforms typically connect to larger lender networks.

What compliance considerations apply to automated loan placement?

Automated placement systems maintain audit trails, support fair lending practices, and meet data security standards like SOC 2. Platforms typically support configurable consent flows and regulatory reporting to address jurisdiction-specific requirements. Fair lending compliance requires that automated rules do not produce discriminatory outcomes, which means regular monitoring of approval rates across protected classes.